Income-Driven Repayment in 2026: How U.S. Student Loan Borrowers Can Navigate IDR, Recertification, and the Return of the Tax Bomb

Published July 15, 2026

The federal student loan system entered 2026 under one of the most consequential restructurings in its history. After more than a decade of shifting rules, court challenges, and a three-year payment pause, the U.S. Department of Education is now enforcing a narrower set of income-driven repayment (IDR) plans, tightening recertification rules, and preparing borrowers for the return of a potential "tax bomb" as older loans approach forgiveness milestones. For the roughly 43 million Americans with federal student debt, understanding how IDR works today is not a theoretical exercise. It determines monthly cash flow, credit health, and, for many, the risk of wage garnishment or lawsuits.

This guide walks through the current IDR landscape, the mechanics of income recertification, how the tax treatment of forgiven balances is expected to change after 2025, and the legal options borrowers have when servicers make mistakes or when hardship makes even reduced payments impossible. Every figure and rule cited below comes from official sources, including Federal Student Aid (studentaid.gov), the Consumer Financial Protection Bureau, and the Internal Revenue Service.

Table of Contents

- The 2026 IDR Landscape at a Glance

- Which IDR Plans Still Exist in 2026

- Annual Recertification: Deadlines, Documents, and Common Mistakes

- The Return of the "Tax Bomb" After 2025

- Servicer Errors and Your Legal Options

- Hardship, Forbearance, and Bankruptcy Discharge

- Where Insurance and Estate Planning Fit In

- When to Involve a Student Loan Attorney

- State-Level Considerations and Consumer Protections

- Frequently Asked Questions

The 2026 IDR Landscape at a Glance

Income-driven repayment was designed to keep federal loan payments affordable relative to a borrower's income and household size. Historically, borrowers had four IDR options: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Income-Contingent Repayment (ICR), and the newer Saving on a Valuable Education (SAVE) plan introduced in 2023.

Following the July 2024 injunction that blocked most SAVE plan benefits and the subsequent August 2025 appellate ruling, the Department of Education began transitioning enrolled borrowers off SAVE. Interest accrual on SAVE resumed on August 1, 2025, according to Federal Student Aid's official notice. By early 2026, borrowers had to choose between IBR, PAYE (still available for those who qualify under legacy rules), ICR, or the standard 10-year plan.

Key 2026 numbers to remember

- Federal poverty guidelines for a family of one in the 48 contiguous states: $15,650 (HHS, 2025).

- Standard IBR payment cap: 15% of discretionary income (10% for borrowers who first borrowed on or after July 1, 2014).

- Forgiveness timeline under IBR: 20 or 25 years depending on loan disbursement date.

- Public Service Loan Forgiveness (PSLF) qualifying period: 120 qualifying monthly payments.

Which IDR Plans Still Exist in 2026

Income-Based Repayment (IBR)

IBR remains the workhorse of income-driven repayment. Payments are capped at 10% of discretionary income for "new borrowers" (those with no outstanding federal student loans as of July 1, 2014, who took out a new loan after that date) and 15% for everyone else. Remaining balances are forgiven after 20 years (new borrowers) or 25 years (older borrowers). IBR is statutory, meaning it is written into the Higher Education Act and cannot be eliminated by administrative action alone.

Pay As You Earn (PAYE)

PAYE also caps payments at 10% of discretionary income and offers forgiveness after 20 years. It has stricter eligibility: borrowers must have taken a new Direct Loan on or after October 1, 2011, and had no outstanding federal loans as of October 1, 2007. New enrollments in PAYE were closed for a period in 2024 but partially reopened in 2025 for borrowers transitioning out of SAVE.

Income-Contingent Repayment (ICR)

ICR is the only IDR plan available to Parent PLUS borrowers who consolidate. Payments equal the lesser of 20% of discretionary income or what would be owed on a fixed 12-year plan adjusted for income. Forgiveness comes after 25 years.

What happened to SAVE

The SAVE plan's 5% cap on undergraduate discretionary income, its no-interest-accrual benefit for on-time payers, and its lower forgiveness threshold for small original balances were the plan's most attractive features. As of early 2026, those benefits are enjoined. Borrowers still technically enrolled in SAVE have been placed into an interest-accruing administrative forbearance while the Department finalizes migration paths.

| Plan | Payment cap | Forgiveness | Available to |

|---|---|---|---|

| IBR (new borrower) | 10% of discretionary income | 20 years | Direct + FFEL after 7/1/2014 |

| IBR (legacy) | 15% of discretionary income | 25 years | All Direct + FFEL |

| PAYE | 10% of discretionary income | 20 years | Direct loans, restrictive eligibility |

| ICR | 20% of discretionary income | 25 years | Direct loans (including consolidated Parent PLUS) |

Annual Recertification: Deadlines, Documents, and Common Mistakes

Every borrower on an IDR plan must recertify income and family size each year. Missing a recertification deadline is one of the most common reasons monthly payments jump unexpectedly, sometimes from under $100 to more than $1,000.

The process itself is straightforward on paper. Borrowers log in at studentaid.gov, complete the IDR application, and either import IRS tax data directly or upload alternative documentation of current income (such as recent pay stubs) if their financial situation has changed since the last tax filing.

Common recertification mistakes

- Recertifying with outdated income. If a borrower lost hours or a job after filing their last tax return, they can (and should) submit alternative documentation.

- Failing to update family size. Marriage, divorce, or the birth of a child changes the discretionary income calculation and can lower monthly payments significantly.

- Ignoring servicer notices. The Department of Education notifies borrowers roughly 60 to 90 days before their recertification deadline. Notices go to the email address on file, which is often outdated.

- Assuming spousal income does not matter. Under IBR and PAYE, filing taxes jointly can dramatically increase the calculated payment. Many married borrowers reduce payments legally by filing separately, though this has its own tax trade-offs.

Practical tip

Set a calendar reminder 45 days before the recertification deadline. That window is enough to gather updated documentation, evaluate whether filing status changes are worthwhile, and correct any address or email issues with the servicer before the automatic payment recalculation kicks in.

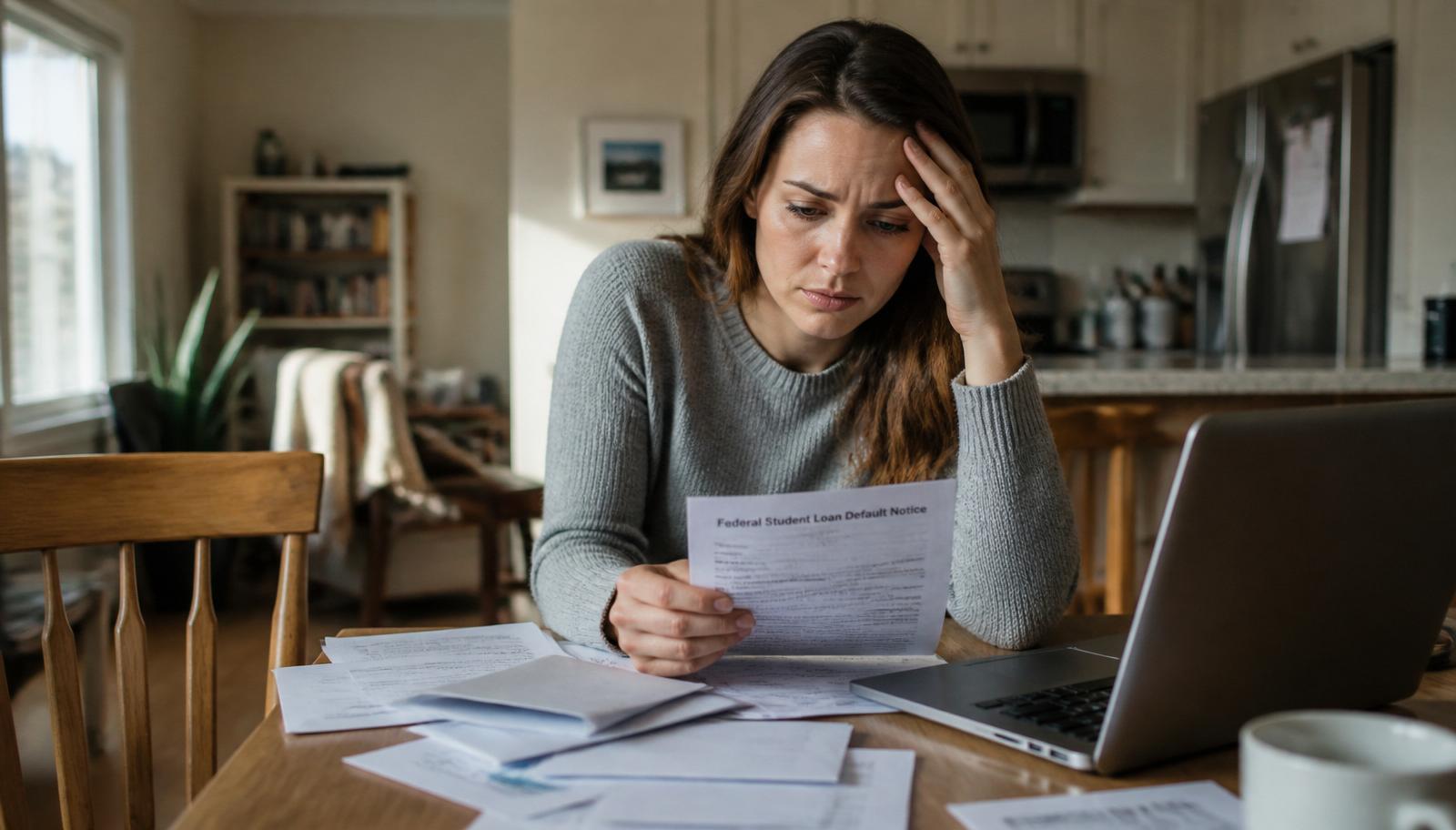

The Return of the "Tax Bomb" After 2025

Under the American Rescue Plan Act of 2021, federal student loan amounts discharged between January 1, 2021 and December 31, 2025 are excluded from federal taxable income. This includes forgiveness under IDR, total and permanent disability discharge, and closed-school discharge.

That exclusion is currently scheduled to expire on December 31, 2025. Unless Congress extends it, IDR forgiveness that occurs in 2026 and beyond could once again be treated as ordinary taxable income at the federal level, per the general rule under IRS Publication 970. State treatment varies: some states already conformed to the federal exclusion, some tax forgiven balances, and others are in flux.

Why the numbers matter

Consider a hypothetical borrower who reaches the 25-year IBR forgiveness point in 2027 with a $70,000 remaining balance. If the exclusion is not extended, that borrower could face a one-time increase in taxable income of $70,000, potentially pushing them into a higher marginal bracket for that year. On a joint return in the 24% bracket, that could translate to roughly $16,800 in additional federal tax owed, plus state taxes where applicable.

Borrowers approaching forgiveness in the next several years should model this scenario with a CPA or enrolled agent well in advance, and evaluate strategies such as accelerating deductible expenses in the forgiveness year, adjusting withholding, or negotiating an IRS Offer in Compromise if the resulting bill creates hardship.

Servicer Errors and Your Legal Options

Federal loan servicers, including MOHELA, Nelnet, EdFinancial, and Aidvantage, have collectively been the subject of hundreds of thousands of complaints filed with the CFPB since 2022. The most frequent issues involve miscounted qualifying payments, incorrect IDR calculations, and delayed processing of PSLF employer certification forms.

Documented rights borrowers have

- The right to request a payment count audit. Under current PSLF and IDR account adjustment procedures, borrowers can ask the Department of Education to review qualifying payment counts.

- The right to file a formal complaint. Complaints can be submitted through the CFPB complaint portal, the Department of Education Ombudsman, or a state attorney general.

- The right to sue for statutory violations. The Fair Credit Reporting Act, the Fair Debt Collection Practices Act, and state consumer protection statutes provide private rights of action when servicers misreport payments or engage in abusive collection practices.

Borrowers who suspect systematic servicer errors should download every account statement, save every email, and keep a written log of phone calls, including the representative's name and confirmation number. This documentation becomes crucial evidence if the matter escalates to litigation or arbitration.

Hardship, Forbearance, and Bankruptcy Discharge

Not every borrower can meet even a reduced IDR payment. In those cases, several options exist. Economic hardship deferment and unemployment deferment can pause payments for up to 36 months combined, and interest does not accrue on subsidized loans during deferment. General forbearance is available for shorter periods but interest continues to accrue on all loan types.

Bankruptcy is no longer as difficult as it was

The joint 2022 guidance from the Department of Justice and the Department of Education created a streamlined process for pursuing federal student loan discharge in bankruptcy. Borrowers file an adversary proceeding, complete an attestation form documenting their financial circumstances, and DOJ attorneys evaluate whether to recommend discharge. According to the DOJ's own reporting, more than 99% of cases filed under the streamlined process through mid-2024 resulted in full or partial discharge.

Bankruptcy is still a serious step with long-term credit consequences, and Chapter 7 or Chapter 13 filings require licensed legal counsel. But the outdated narrative that "student loans can never be discharged in bankruptcy" is factually incorrect under current guidance.

Where Insurance and Estate Planning Fit In

Federal student loans generally discharge upon the borrower's death, and Parent PLUS loans discharge upon the death of either the parent borrower or the student on whose behalf the loan was taken. Private student loans, by contrast, may or may not discharge at death depending on the lender's policy and applicable state law.

For borrowers with private loans or co-signers, term life insurance sized to the outstanding balance is a common risk-mitigation strategy discussed in our overview of life insurance basics. Estate planning attorneys often recommend that borrowers with substantial student debt document loan balances and co-signer information in their estate records, so survivors can quickly notify lenders and request discharge or hardship review.

Disability is a separate risk. Federal loans can be discharged under Total and Permanent Disability (TPD) provisions when documented by the Social Security Administration, the Department of Veterans Affairs, or a physician. Long-term disability insurance from an employer or private carrier can bridge the gap while a TPD application is processed.

When to Involve a Student Loan Attorney

Not every problem requires legal counsel. Recertification errors, incorrect family size entries, and typical account questions can usually be resolved by escalating through the servicer, the Department of Education Ombudsman, and the CFPB. But certain scenarios warrant a consultation with an attorney experienced in consumer finance or education law:

- A servicer refuses to correct a documented payment count error after a formal complaint.

- Wage garnishment or Treasury offset has begun on a loan the borrower believes is in good standing or eligible for rehabilitation.

- A borrower is being sued by a private lender or a collection agency.

- Bankruptcy is being considered and the borrower has both federal and private education debt.

- A borrower is denied PSLF forgiveness despite documented qualifying employment.

Related legal frameworks that often intersect with student loan disputes are discussed in our guides to wrongful termination laws (relevant when job loss triggers a hardship deferment) and student loan default and wage garnishment.

State-Level Considerations and Consumer Protections

Federal rules set the floor for student loan servicing, but a growing number of states have layered their own consumer protection statutes on top. As of 2026, more than a dozen states, including California, Illinois, Washington, New York, Colorado, Connecticut, Massachusetts, Maine, Nevada, New Jersey, Virginia, and Minnesota, have enacted student loan borrower bills of rights or licensed servicers under state law.

These statutes typically require servicers to respond to written borrower inquiries within a defined window (often 30 days), prohibit misleading statements about loan status or forgiveness eligibility, and grant the state attorney general authority to investigate patterns of servicing abuse. Borrowers who cannot get satisfactory answers from a federal servicer often obtain faster results by filing a parallel complaint with the state regulator that licenses that servicer.

State ombudsman offices, where they exist, can also help borrowers reconstruct payment histories, verify PSLF employer eligibility, and navigate discharge applications for total and permanent disability or closed-school cases. Contact information for state ombudsmen is generally listed on the state attorney general's website.

Public-service employers and PSLF nuances

Borrowers pursuing Public Service Loan Forgiveness should be aware that the definition of a qualifying employer has narrowed and broadened multiple times since PSLF's inception in 2007. As of early 2026, qualifying employers generally include federal, state, local, and tribal government agencies, plus 501(c)(3) nonprofit organizations. Full-time employment is defined as at least 30 hours per week, or the employer's own full-time threshold if higher. Time spent on employer-approved paid leave counts as qualifying employment. Borrowers should re-certify employment annually using the official PSLF form, even if they are not yet at the 120-payment threshold, so that any counting errors can be identified and corrected years before forgiveness eligibility.

Frequently Asked Questions

What is the difference between income-driven repayment and the standard 10-year plan?

The standard 10-year plan sets a fixed monthly payment large enough to fully amortize the loan over 120 months. Income-driven repayment ties payments to income and household size, extending the term to 20 or 25 years with forgiveness of any remaining balance at the end.

How is discretionary income calculated in 2026?

For IBR and PAYE, discretionary income equals the borrower's adjusted gross income minus 150% of the federal poverty guideline for the borrower's family size and state. For ICR, the threshold is 100% of the poverty guideline.

Do I have to switch off SAVE?

Borrowers currently in SAVE will not remain there indefinitely. Federal Student Aid has announced a phased transition to IBR or, where eligible, PAYE. Borrowers should watch for official notices and confirm through studentaid.gov before making changes.

Will forgiven balances be taxed in 2026?

Unless Congress extends the American Rescue Plan Act exclusion, forgiven federal student loan balances discharged after December 31, 2025, may again be treated as ordinary income at the federal level. State treatment varies.

Can I switch IDR plans mid-year?

Yes. Borrowers can switch IDR plans at any time, subject to eligibility. Switching typically triggers a recalculation and a new recertification date, and can also capitalize accrued interest depending on the transition.

Does marriage always raise my payment?

Not automatically. Under IBR and PAYE, filing taxes as married filing separately generally excludes spousal income from the payment calculation. Under ICR, spousal income counts regardless of filing status.

What happens if I never recertify?

Missing recertification typically causes the payment to reset to what a standard 10-year plan payment would be based on the original loan balance and term. Unpaid interest may also capitalize, increasing the total balance owed.

Are private student loans eligible for IDR?

No. IDR is a federal loan program. Private lenders offer their own hardship programs, refinancing options, and settlement negotiations, but the federal IDR framework does not apply.

Disclaimer: This article is for general informational purposes only and does not constitute legal, tax, or financial advice. Loan rules, tax treatment, and administrative procedures change frequently. Borrowers should consult a licensed attorney, certified public accountant, or the U.S. Department of Education directly before making decisions that affect their federal student loans. All third-party statistics and rules cited are current as of publication and drawn from official government sources.

Related Articles

COBRA Health Insurance in 2026: Coverage Rules, Costs, and Legal Rights for U.S. Workers After Job Loss

A source-based 2026 guide to COBRA continuation coverage: qualifying events, election deadlines, true premium costs, ACA alternatives, employer notice duties, and enforcement of ERISA rights.

Medicare Advantage Denials in 2026: How to Appeal Prior Authorization Rejections and Protect Your Coverage

A neutral, source-based 2026 guide to Medicare Advantage denials: prior authorization rules, the five-level appeal process, expedited review, new CMS coverage rules, and when to hire an elder-law attorney.

Student Loan Default in 2026: Wage Garnishment, Credit Damage, and How U.S. Borrowers Can Legally Recover

A neutral, source-based 2026 guide to federal student loan default in the United States: wage garnishment rules, Treasury offset, credit damage, rehabilitation, consolidation, and when to hire a consumer-rights attorney.

FAFSA 2026-2027: Student Aid Index, Pell Grant Expansion, and How to File for Maximum Aid

A neutral 2026-2027 FAFSA guide covering the new Student Aid Index, expanded Pell Grant eligibility, the contributor model, required documents, and step-by-step filing procedures.