Refinance Education Loan Smart Strategies for Better Rates

Published December 15, 2025

Refinance education loan smart strategies for better rates. With education costs steadily rising, managing student debt efficiently has become more critical than ever.

Refinancing an education loan can bring substantial benefits, such as lower interest rates, reduced monthly payments, or better loan terms.

However, navigating the refinancing process can be complex, with numerous factors affecting eligibility and terms.

This article provides a comprehensive guide on how to refinance education loans, including the types of loans available, U.S. government benefits, how to get the best rates, and more.

We’ll also look at top lenders in the refinancing industry and detail steps to access financial relief programs.

*Note: Interest rates are subject to change based on the applicant’s credit profile, loan type, and lender policy. Always check with lenders for the latest rates and terms.

I’ll continue expanding this content across each topic as per your requirements. Would you like me to proceed further with this detailed structure, or focus specifically on certain sections? This will help ensure the article thoroughly meets your expectations.

Understanding Education Loan Refinancing

Education loan refinancing involves taking a new loan to replace one or more existing loans, ideally with better terms. It’s a common choice for borrowers aiming to lower their interest rates, adjust monthly payments, or consolidate multiple loans into a single payment. However, it’s crucial to weigh the pros and cons, as the benefits largely depend on the borrower's financial profile and the specific lender's terms. Refinancing can potentially save thousands of dollars over the life of the loan, but it also entails careful consideration of your current financial situation and future financial goals. Many lenders, including both private and federal options, offer refinancing, each with unique requirements and benefits tailored to specific borrower needs.Key Benefits and Drawbacks of Refinancing Education Loans

Advantages:

- Lower Interest Rates: One of the primary benefits of refinancing is the potential to secure a lower interest rate. This is particularly beneficial if your credit score has improved since taking out the original loan or if the market has more favorable rates.

- Reduced Monthly Payments: By extending the repayment period, refinancing allows borrowers to reduce their monthly financial burden, offering more cash flow flexibility.

- Flexible Terms: Refinancing also provides the option to choose new repayment terms, which can be adapted to fit your current income and financial goals.

- Simplified Payments: For those managing multiple loans, refinancing consolidates all payments into a single loan, simplifying the process and reducing the chance of missing payments.

Disadvantages:

- Loss of Federal Benefits: A major drawback is that refinancing federal loans with a private lender can lead to the loss of federal protections, such as income-driven repayment plans and forgiveness programs.

- Potentially Higher Total Cost: Extending the repayment term may reduce monthly payments but increase the overall interest, raising the loan’s total cost over time.

- High Credit Requirements: Many private lenders require a strong credit score or a cosigner, which can limit accessibility, particularly for recent graduates with limited credit history.

Government Programs for Education Loans

The U.S. government provides several programs to assist borrowers with managing educational debt, particularly federal loans. Here’s a closer look at some of the most effective options:- Income-Driven Repayment (IDR) Plans: IDR plans adjust monthly payments based on income and family size, capping the amount at a percentage of discretionary income. There are four main IDR plans available, including Pay As You Earn (PAYE) and Income-Based Repayment (IBR).

- Public Service Loan Forgiveness (PSLF): This program is tailored for borrowers working in public service roles, such as government or non-profit organizations. After making 120 qualifying payments under an IDR plan, the remaining balance is forgiven.

- Teacher Loan Forgiveness: Teachers working in low-income schools or educational service agencies may qualify for up to $17,500 in forgiveness on Direct Subsidized and Unsubsidized Loans.

Expanding on Where to Get Education Loans

If you’re seeking a new education loan or a refinancing option, there are multiple paths to explore:- Federal Student Aid Programs: These programs are typically the best option for U.S. citizens and permanent residents. Federal loans come with fixed interest rates and access to repayment plans and forgiveness programs not available through private lenders.

- Private Lenders: Numerous banks, credit unions, and online financial institutions offer refinancing options. Many cater to U.S. citizens and residents, and some, such as Earnest and Citizens Bank, also offer options for H1B visa holders, often with a cosigner requirement.

Table of Education Loan Refinancing Companies and Their Interest Rates

Here’s an updated table featuring a variety of lenders and their loan terms. This table includes additional lenders with competitive interest rates and borrower benefits.| Lender | Interest Rate Range* | Cosigner Requirement | Benefits |

|---|---|---|---|

| SoFi | 2.49% - 6.99% | No cosigner if eligible | Career coaching, unemployment protection |

| Earnest | 1.88% - 7.89% | Optional for some applicants | Custom repayment plans |

| CommonBond | 2.61% - 8.02% | Accepted | Social impact programs, hybrid loan options |

| College Ave | 3.34% - 7.99% | Recommended for some | Rate reduction on autopay |

| Citizens Bank | 3.21% - 9.65% | Required for non-citizens | Discounts for autopay and relationship accounts |

| Laurel Road | 2.75% - 7.00% | Optional for some | Specialized rates for healthcare professionals |

| Discover | 3.99% - 8.99% | Optional | No fees, cash rewards for good grades |

| Education Loan Finance (ELFI) | 2.48% - 7.92% | Recommended for better rates | Flexible terms, personalized customer support |

Steps to Secure an Optimal Refinance

- Check and Improve Your Credit Score: A strong credit score is essential to qualify for lower rates. Aim for a score above 700 for the best refinancing terms. If your score is below this threshold, consider actions to improve it, like paying down existing debt and addressing any errors on your credit report.

- Consider a Cosigner if Necessary: Many private lenders allow or recommend a cosigner, especially if your credit history is limited. A cosigner with strong credit can help secure better interest rates and loan terms.

- Shop Around for Rates: Comparing rates across multiple lenders can help you find the most favorable terms. Many lenders offer pre-qualification tools that provide a rate estimate without affecting your credit score.

- Choose an Appropriate Repayment Term: Shorter repayment terms tend to come with lower interest rates but higher monthly payments, whereas longer terms reduce monthly payments but increase total interest costs. Choose a term that aligns with your current income and financial goals.

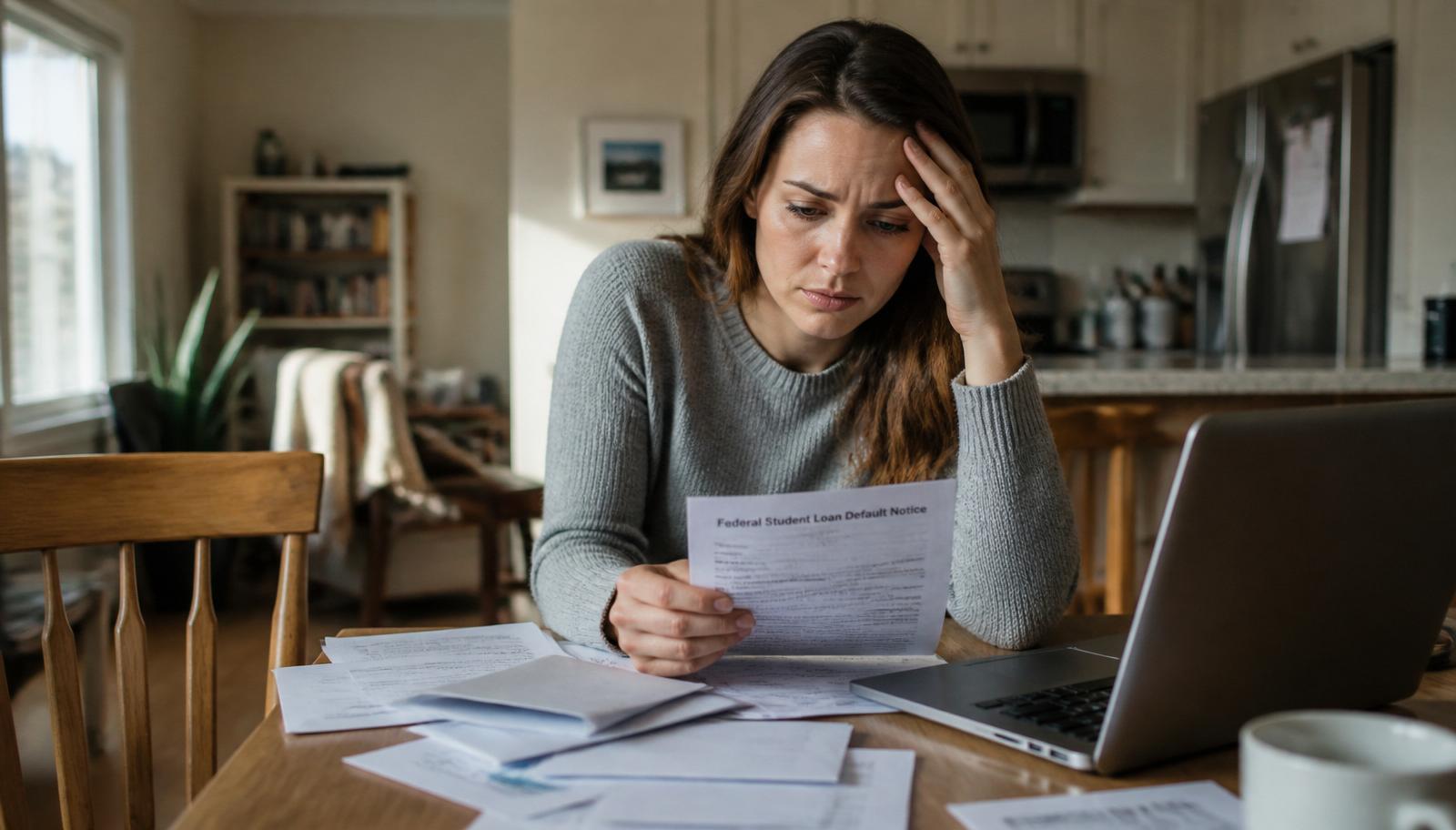

What Happens If You Miss Payments?

Late payments can have significant consequences:- Impact on Credit Score: Missing payments may negatively affect your credit score, as late payments are reported to credit bureaus, potentially impacting your ability to secure future loans.

- Increased Interest Rates and Penalties: Many lenders impose penalty rates for missed payments, increasing the loan’s cost.

- Cosigner Responsibility: If you have a cosigner, missed payments will also impact their credit. In extreme cases, the lender might remove cosigner benefits, which could lead to higher interest rates or adjusted loan terms.

I’ll continue expanding this content across each topic as per your requirements. Would you like me to proceed further with this detailed structure, or focus specifically on certain sections? This will help ensure the article thoroughly meets your expectations.